Estimated Reading Time: 5 minutes

Pay Less for Health Insurance — Without Reducing Your Protection.

Health insurance premiums don’t have to keep increasing every year.

Many people overpay simply because they don’t know the legal and smart ways to reduce their premium — without compromising coverage.

This guide explains how to lower your health insurance cost the right way, not through risky shortcuts.

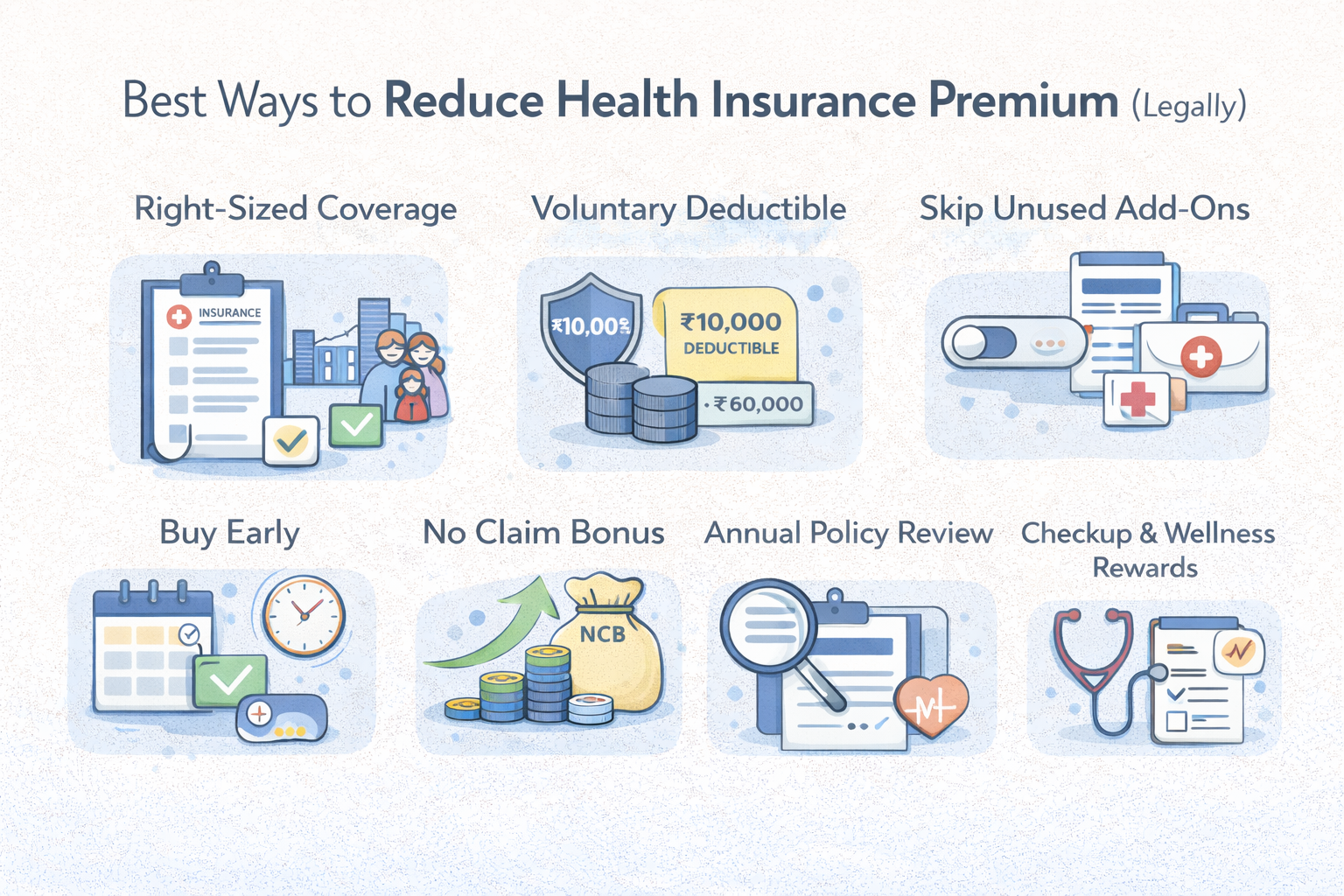

Choose the Right Coverage Amount (Not the Highest)

More coverage isn’t always better.

Buying a very high sum insured when you don’t need it leads to unnecessary premium costs.

✔ Choose coverage based on:

- City of residence

- Family size

- Age and health conditions

- Existing employer coverage

Right-sizing your coverage saves money immediately.

Opt for a Voluntary Deductible

A voluntary deductible means you agree to pay a small part of the bill in exchange for a lower premium.

Best suited for:

- Young individuals

- Families with emergency savings

- Those with low claim history

👉 Higher deductible = Lower premium (legally).

Avoid Unnecessary Add-Ons

Some add-ons sound attractive but are rarely used.

Commonly overpaid riders:

- Hospital cash benefits

- Duplicate coverage already provided elsewhere

- Minor outpatient riders with limits

Add-ons should match real risk, not marketing appeal.

Buy Early (Age Matters)

Premiums increase with age.

Buying health insurance earlier:

- Locks lower premium

- Reduces waiting periods

- Improves long-term affordability

Waiting even 3–5 years can significantly increase lifetime costs.

Maintain a No-Claim History

If you don’t claim:

- You earn a No Claim Bonus (NCB)

- Your coverage increases or premium reduces

- Avoid small, unnecessary claims when possible

Small claims cost more in the long run.

Review Your Policy Every Year

Renewal is not the same as review.

At renewal:

- Check if coverage still matches needs

- Remove unused riders

- Adjust deductible if needed

Many people overpay simply by auto-renewing blindly.

Common Mistakes to Avoid

- Reducing coverage just to save premium

- Switching policies frequently

- Ignoring waiting periods while switching

- Buying cheapest plans without understanding cost-sharing

Smart savings are planned, not rushed.

How InsuranceConsultationPro.com Helps

✔ Identifies unnecessary premium leaks

✔ Matches coverage to real needs

✔ Helps you save legally

✔ No selling, no pressure

✔ Completely free consultation

Final Word

Reducing your health insurance premium doesn’t mean reducing protection.

With the right strategy, you can pay less, stay covered, and avoid future surprises.

Always optimise — never compromise.