Estimated Reading Time: 5 minutes

If You Don’t Understand These, Your Claim Might Surprise You.

Many people believe health insurance means everything is covered.

In reality, how much you pay during a claim depends on three critical terms:

Deductible, Copay, and Waiting Period.

Misunderstanding these is one of the biggest reasons people feel disappointed during claims. Let’s simplify them — without jargon.

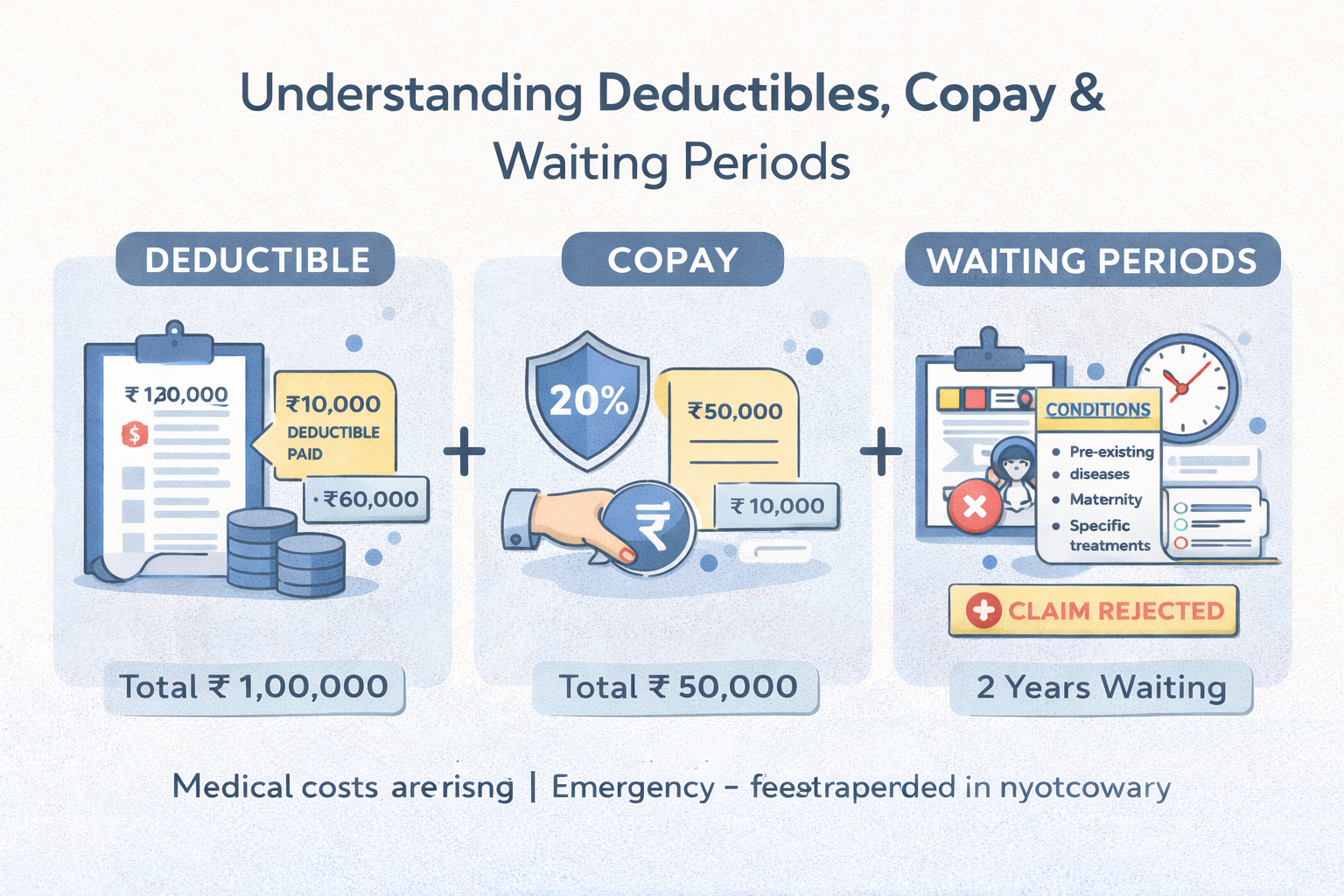

1. What Is a Deductible?

A deductible is the amount you must pay from your own pocket before your insurance starts paying.

Simple example:

- Hospital bill: ₹1,00,000

- Deductible: ₹10,000

- Insurance pays: ₹90,000

Key thing to remember:

- Higher deductible → Lower premium

- Lower deductible → Higher premium

Deductibles are best chosen based on how much you can comfortably pay in an emergency.

2. What Is a Copay?

A copay is a percentage or fixed amount you share every time you make a claim.

Example:

- Copay: 20%

- Bill: ₹50,000

- You pay: ₹10,000

- Insurance pays: ₹40,000

Copay applies even after the deductible is paid.

👉 Policies with copay usually have lower premiums, but higher out-of-pocket costs during treatment.

3. What Is a Waiting Period?

A waiting period is the time you must wait before certain benefits become active.

Common waiting periods apply to:

- Pre-existing diseases

- Maternity benefits

- Specific treatments or surgeries

Important:

Claims during the waiting period are usually rejected, even if the policy is active.

Why These Three Matter More Than Premium

Many buyers focus only on premium and coverage amount — but these three decide:

- How much you actually pay during a claim

- Whether your claim is approved

- How useful the policy really is

A low-premium policy with high deductibles and copays may cost more when you need it most.

Common Mistakes Buyers Make

- Ignoring deductibles and copays

- Not checking waiting periods

- Assuming employer insurance has no waiting rules

- Buying cheap plans without reading fine print

These mistakes are avoidable with basic awareness.

How to Choose the Right Balance

There’s no one-size-fits-all answer.

Choose:

- Low deductible → if you want minimal out-of-pocket expense

- Higher deductible → if you want lower premium and can manage emergencies

- Shorter waiting period → if you need coverage sooner

A consultation helps align this with your health and finances.

How InsuranceConsultationPro.com Helps

✔ Explains policy terms in plain language

✔ Helps estimate real out-of-pocket costs

✔ Prevents claim-time surprises

✔ 100% free, no selling, no pressure

Final Word

Health insurance works best when you understand how costs are shared.

Deductibles, copays, and waiting periods aren’t tricks — they’re rules.

Once you understand them, choosing the right policy becomes easy and stress-free.